Wealth inequality in the United States is a pressing issue that has been steadily worsening over the past few decades. The concentration of wealth among the richest individuals contrasts sharply with the shrinking share held by middle and lower-income groups. This disparity reflects deeper systemic issues that have far-reaching implications for economic stability and social justice.

Addressing Wealth Inequality

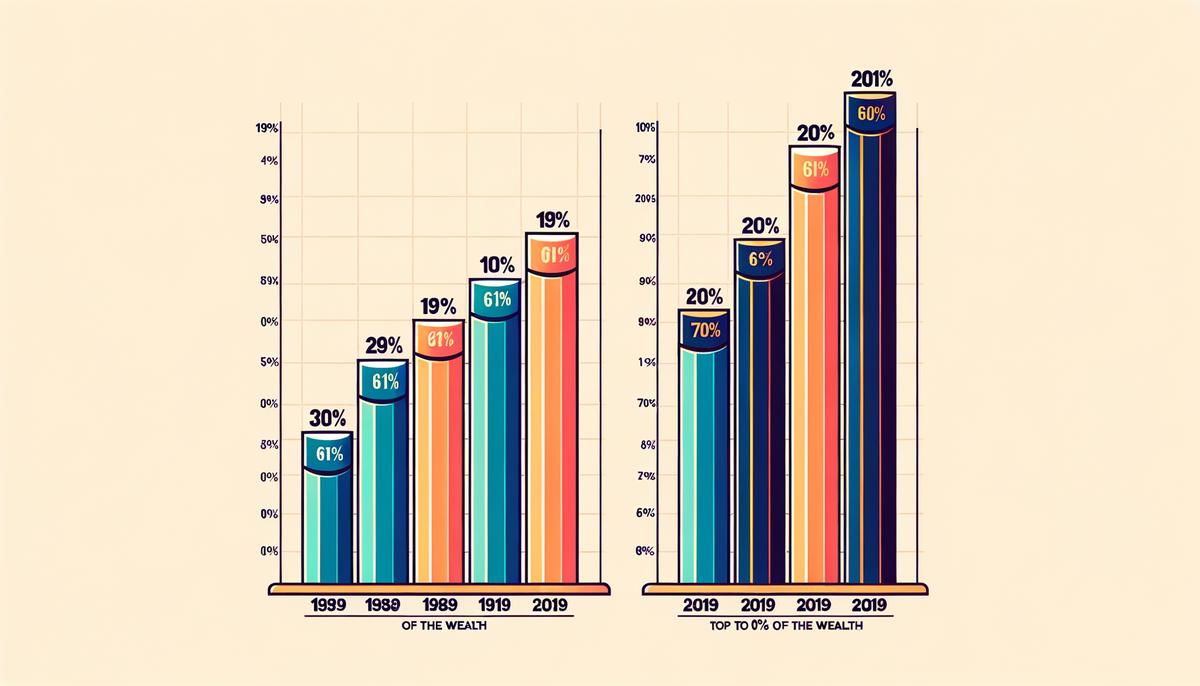

From 1989 to 2019, the wealth share of the richest 10 percent in the U.S. grew from 61 to 70 percent, while the middle and bottom 50 percent saw their wealth shares shrink. Capital gains—taxed at lower rates than wages—account for nearly 22 percent of the pre-tax income for the top 1 percent, compared to less than 1 percent for the bottom and middle income groups.

The Gini coefficient, a measure of inequality, rose from 0.41 in 1979 to 0.51 in 2016 before taxes and transfers. Even after adjustments, it climbed from 0.35 to 0.42. The skewed tax system is a significant factor, with estate taxes only applying to estates valued over $11.4 million, affecting fewer than 0.1 percent of all decedents.

Recent tax cuts have often benefited the wealthy more. The 2017 Trump tax cuts, for instance, projected an average $61,090 cut for households in the top 1 percent, while those in the bottom quintile saw a $70 reduction. Trickle-down economics has failed to uplift the working class while disproportionately benefiting the affluent.

A wealth tax could address this situation. Economists estimate that a wealth tax with a $50 million threshold would affect only 0.06 percent of all U.S. households. This could fund initiatives aiding lower-income Americans and make the tax system more progressive. A 1 percent wealth tax on assets above $50 million could raise $94 billion annually, even accounting for some evasions.

Norway, Spain, and Switzerland employ wealth taxes with varying success. Spain's wealth tax represents 0.5 percent of total revenues, Norway's 1.5 percent, and Switzerland's 4.8 percent. If the U.S. could leverage a similar percentage, it could raise substantial additional revenue.

A well-designed wealth tax could help level the playing field, addressing gaps left by historic tax cuts and trickle-down policies that primarily benefited the wealthy.

Economic Effects and Revenue Generation

The economic effects and revenue-generating potential of a wealth tax are significant. While critics claim it might disincentivize investment and innovation, evidence from countries like Norway and Switzerland suggests otherwise. A well-calibrated wealth tax can promote economic dynamism by encouraging productive investment of assets.

The revenue from wealth taxes can finance public investments in:

- Infrastructure

- Education

- Healthcare

These investments can catalyze long-term economic growth, boost business efficiency, drive innovation and productivity, and enhance the overall quality of life, leading to a more robust workforce.

Wealth taxes can play a crucial role in leveling the economic playing field. The additional revenues can fund social programs that directly benefit lower and middle-income households, such as:

- Enhancing the Earned Income Tax Credit

- Funding universal pre-K education

- Expanding affordable housing initiatives

The efficiency of wealth taxes compared to other forms of taxation is noteworthy. Traditional income taxes, often skewed by loopholes and preferential treatments, fall short in taxing the wealthiest effectively. Wealth taxes, focusing on net worth, can circumvent such pitfalls.

A wealth tax is progressive by nature, designed to impose a heavier burden on those with greater financial resources. This contrasts with consumption taxes, which disproportionately affect lower-income households.

Adopting a wealth tax isn't about penalizing success; it's about ensuring that success furthers the common good. It's about building an economy where prosperity is shared, and opportunity is accessible to all, not just the privileged few.

Challenges and Legal Aspects

Implementing a wealth tax in the United States faces practical and legal challenges. Tax evasion is a significant concern, as wealthy individuals have the means to engage in sophisticated tax planning strategies. To combat this, the U.S. would need a highly effective and well-funded Internal Revenue Service (IRS), capable of tracking and valuing diverse asset classes accurately.

Enforcing a wealth tax would require international cooperation to curb tax evasion effectively. Countries like Norway and Switzerland tackle this issue through international tax treaties and information-sharing agreements. The U.S. would need to engage actively with international bodies to build a system resistant to evasive maneuvers.

Administrative difficulties pose a notable hurdle. Unlike income, net worth involves a wide array of assets that fluctuate in value. Establishing a fair and consistent baseline for valuation each year is complex. A practical solution would be to set clear guidelines and standardized methods for asset valuation, similar to approaches used in Norway and Spain.

The constitutional debate is another challenge. The U.S. Constitution requires that direct taxes be apportioned among the states based on population, which some argue would make a wealth tax unviable without significant changes.

Supporters suggest that a wealth tax could be framed to avoid these constitutional constraints, possibly as an excise tax or another form of permissible levy.

European examples provide mixed lessons:

- Spain has faced challenges with compliance and administration but persists due to perceived equity benefits.

- Norway's experience has shown that even at lower thresholds, wealth taxes can work but require constant refinement and public support.

- Switzerland's local-level implementation offers insights into decentralization as a solution to administrative complexity.

The journey towards implementing a fair and effective wealth tax in the U.S. is fraught with obstacles, yet not insurmountable. Through careful planning, international cooperation, administrative rigor, and possibly constitutional clarity, we can work towards a more just and equitable tax system.

Social and Moral Justification

Wealth taxes are rooted in our social and moral fabric, representing a step towards addressing systemic injustices and promoting economic equity. In our society, wealth often reflects deeper, historical inequalities. For centuries, systemic barriers have prevented marginalized communities from accumulating wealth at the same rate as their white counterparts. Policies like slavery, Jim Crow laws, redlining, and discriminatory labor practices have disproportionately benefited white households while oppressing minority communities. This legacy is evident in today's racial wealth gap, where:

- The typical white family has eight times the wealth of the average Black family

- The typical white family has five times the wealth of the average Latinx family

A wealth tax provides an avenue for addressing these historical injustices. By implementing this tax and redirecting revenues into targeted programs for economic upliftment, we can make wealth redistribution a tool for systemic change. This approach aligns with the moral imperative of equity, ensuring that society's prosperity benefits all its members.

Historical examples support the argument for wealth redistribution as a social necessity. The post-World War II era in the United States, characterized by progressive tax policies and expansive public programs, contributed to a more equitable society. This high-tax era wasn't merely a financial decision; it was a moral stance that wealth should contribute to the collective good.

In today's context, social movements like Black Lives Matter, Occupy Wall Street, and the "Yellow Vest" protests underscore a global demand for economic justice. Implementing a wealth tax is a proactive response to this growing discontent, acknowledging the grievances of those marginalized by economic disparities.

The theoretical basis for a wealth tax as a moral necessity can be found in various ethical frameworks:

- John Rawls' theory of justice posits that a fair society is one where inequalities are arranged to benefit the least advantaged.

- Amartya Sen's capability approach emphasizes the importance of enabling all individuals to achieve their potential.

The ethical dimensions of wealth redistribution also intersect with religious and cultural values that emphasize charity, community, and stewardship. Many world religions and philosophies promote the idea that those with great wealth have a duty to support the wider community. Wealth taxes institutionalize this principle, ensuring that support isn't left to voluntary contributions but integrated into our fiscal policies.

"Implementing a wealth tax is not just an economic tool; it's a pathway to justice and a means of addressing deep-seated inequities. By redistributing wealth more equitably, we can foster a sense of community, reduce social unrest, and promote a fairer, more inclusive society."

Addressing wealth inequality through measures like a wealth tax is both an economic necessity and a moral imperative. By redistributing resources more equitably, we can foster a society where prosperity benefits everyone, not just the privileged few. This approach aligns with our core values of justice and equality, paving the way for a fairer future where opportunity is accessible to all.